Addressing the ‘state’ of the midterms, economy and markets

Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways

- Betting markets currently reflect that Democrats will flip the House

- Despite depressed confidence, the US economy remains on solid footing

- A muted start to the year for the S&P 500, but fundamentals are strong

President Donald Trump is set to deliver the first State of the Union address of his second term to a joint session of Congress on Feb. 24, 2026. While the Supreme Court’s IEEPA decision and a partial government shutdown may hang over the highly anticipated speech, the president is still expected to spotlight several policy achievements from the first year of his second term. Chief among them are the passage of the One Big Beautiful Bill Act, which is widely expected to generate sizable tax refunds for households this year, and sweeping changes to US trade policy. Markets will be listening closely for clues about the administration’s key legislative priorities over the next three years, as well as any broader initiatives heading into November’s midterm elections. In the spirit of the State of the Union, we share below our own take on the current “state” of the upcoming midterm election, the economy and financial markets.

State of midterm elections

It’s been a busy start to the midterm election year in Washington, marked by a second government shutdown, rising geopolitical tensions - including Iran and Venezuela – and continued uncertainty around tariffs. While the economy has so far held up well, President Trump’s approval rating has moved in the opposite direction, slipping to ~41%. That’s near the low point of his current term and roughly in line with where it stood at this stage of his first term. Historically, presidential approval ratings have been closely linked to changes in House seats during midterm elections. Reflecting that, betting markets now assign an 84% probability that Democrats take control of the House, along with a rising – now 40% – probability that the Senate flips as well. With roughly 250 days until election day and the economy and cost of living topping voters’ concerns, affordability is likely to remain front and center for the administration. While many proposed measures, such as the credit card interest rate cap, would require congressional action, the Trump administration is expected to maintain its focus on lowering health care, energy and housing costs.

State of the economy

Even as consumer confidence has slipped to a 12‑year low, the US economy continues to grow at a healthy pace. Strong business investment, especially in the tech sector, along with resilient consumer spending has kept momentum intact. That said, concerns about the labor market haven’t disappeared. Job growth stalled in 2025, with the economy adding just 181,000 jobs, though the unemployment rate remains a historically low 4.4%. Many companies, rather than hiring aggressively, are focusing on boosting productivity with their existing workforce as they adapt to the AI transition. Inflation, meanwhile, has stayed stubbornly above the Fed’s 2.0% target for a fifth straight year, but once the effects of tariffs fade, likely around midyear, we expect the disinflationary trend to resume. Looking ahead, economic growth should remain on solid footing, supported by favorable financial conditions, one expected Federal Reserve (Fed) rate cut this year, fiscal stimulus from the One Big Beautiful Bill tax changes and continued strength in capital spending. In fact, mega‑cap tech investment is projected to jump ~50% in 2026. These factors underpin our economists' forecast for 2.4% growth next year.

State of the bond market

Even as growth shows modest signs of improvement, highlighted by a recent jump in the Citi Economic Surprise Index, front‑end Treasury yields have broken from their typically tight relationship with that measure and moved lower. We see two main reasons for this shift. First, a softer than expected CPI report, likely distorted by last year’s six‑week government shutdown, sparked a sharp rally in Treasuries as markets briefly priced in more than a 50% chance of a third 25‑basis point Fed rate cut, a view that is now fading. Second, rising fears around AI‑driven disruption have unsettled parts of the equity market, increasing the safe‑haven appeal of Treasuries. The move has been swift: two‑year yields recently fell to their lowest level in nearly four years, while the 10‑year dropped to 4.07%, down ~16 basis points montu-to-date – its steepest monthly decline since last February. In our view, this looks overdone. With growth expected to firm and a Fed cut already priced in, we see the 10‑year Treasury yield rising back toward the 4.25%–4.50% range by year‑end.

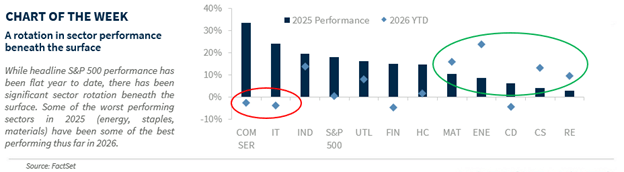

State of the equity market

After strong gains in 2025 (+18%), equity markets have gotten off to a quieter start this year. At the headline level, the S&P 500 is up just 0.4%, its weakest opening since 2022. Beneath the surface, though, there’s been plenty of action, with pronounced sector rotation driving returns. Many of last year’s laggards – energy, consumer staples and materials – have emerged as this year’s leaders, while last year’s standouts, including tech and communication services, are now trailing. Dispersion within sectors has also been elevated, as AI‑related disruption fears have created perceived winners and losers – for example, semiconductors are significantly outperforming software within tech. Looking ahead, with fundamentals still supportive, earnings trending higher and Fed policy remaining accommodative, we expect the bull market to continue. That said, stretched valuations and elevated sentiment point to more volatility and modest gains. We see the S&P 500 ending the year near 7,250 and favor tech, industrials, consumer discretionary and healthcare.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.